Current Economic Statistics and Review For the

Week

Ended September 2, 2006

Theme

of the week:

Growing Income Inequality: India’s Experience in the Nineties*

"Issues of equity and social cohesion (are) issues that affect the very temperament of the country. We are forced to face the question of whether we will be able to go forward together as a unified society with a confident outlook or as a society of diverse economic groups suspicious of both the future and each other." William McDonough (Chairman, Federal Reserve Bank of New York, 1998)

Introduction

Popular opinion assumes a reduction in poverty and the bridging of income inequalities to be a direct consequence of, or rather analogous to, improved economic growth; yet, several instances of the contrary being true have given rise to a plethora of economic literature questioning the nature of the relationship between economic growth and reduced income inequalities. An analysis of data for the post-reform period in India confirms the conception that economic reforms lead to higher economic growth, yet as we extend the analysis, there are distinctive signs of increasing inequality in income distribution – though the absolute income levels have witnessed a rise for almost all employees, the gap between the relative incomes of the high-income and low-income groups seems to be widening. Within the framework of a liberalised economy, if the impact and extent of this increasing inequality is to be contained, there is a definitive case for social security measures in the form of both legislative interventions by the government as well as social responsibility initiatives by the private sector that has begun to play a direct and active role in the growth process.

I

Brief

Review of Literature

The nature of relationship between inequality and growth has remained debatable as many economists have put forward varied results. The starting point of the literature linking economic development and income inequality dates to the well-known works of two Nobel Prize winners, W.Arthur Lewis (1954) and Simon Kuznets (1955). Lewis, in his classic 1954 article “Economic Development with Unlimited Supplies of Labour,” developed a theoretical model in which growth and accumulation in a dual economy would start in the modern industrial sector, wherein capitalists would hire at a given wage and reinvest a share of their profits and the number of traditional agricultural labourers willing to move to this high-productivity, high-wage sector would be unlimited. In this process of development, and as long as these assumptions would prevail, inequality in the distribution of income would increase as average incomes rose. Eventually there would be a turning point after which inequality would fall as the surplus labor phase would come to an end and the dualistic economy would be replaced by a single-sector, fully industrialized economy. Although Kuznets did not explicitly model the inter-sectoral shifts of population as part of the development process, he did build on them to articulate his basic idea of an inverted-U relationship between economic growth and income inequality (the “Kuznets curve”). However, the data available at that time, and those used by Kuznets for empirical backing of his argument had several limitations and he was well aware of them, in his own words, “5 percent of empirical information and 95 per cent speculation, some of it possibly tainted by wishful thinking.” Kuznets based his speculation primarily on longitudinal data and called for in-depth case studies of the economic growth of nations. But many subsequent studies simply used aggregate cross-country data (often not particularly of high quality) and reduced-form models to explore and support the hypothesis of an inevitable trade off between economic growth and equity.

In the post-reform period, it has been typically argued that the chain of causation runs from economic growth to inequality. Economic reforms and the consequent higher economic growth have led to enhancements in capital accumulation which, in turn, are occasioned by better returns to capital and a shift in the remuneration structure from labour to capital at least in the initial phases of reforms. But there is ample reason to believe that the causality might be from inequality to growth as well, Persson and Tabellini (1993) propose that inequality is harmful to growth. But Fishlow (1995) finds no such link in case of Latin American countries; on the other hand, Bruno, Ravallion and Squaire (1996) conclude “initial distribution matters to the extent of nature of subsequent growth”. Redistributive policies that increase people’s access to credit markets and their opportunity to invest, for example, would contribute to grow.

In

case of

II

Macroeconomic Performance

The

Indian economy has continued to display significant improvements in

macroeconomic parameters and is being considered to be among the top

growing economies of the world second only to

|

Table

1: Broad Macroeconomic Indicators (in

per cent) |

|||||||||

|

|

1980-81 |

1990-91 |

1995-96 |

2000-01 |

2001-02 |

2002-03 |

2003-04 |

2004-05 |

2005-06 |

|

GDP

at factor cost (1993-94=100)* |

7.2 |

5.6 |

7.3 |

4.4 |

5.8 |

3.8 |

8.5 |

7.5 |

8.4 |

|

GNP

at factor cost (base year =1993-94)* |

7.3 |

5.5 |

7.5 |

4 |

5.9 |

3.9 |

8.6 |

7.6 |

8 |

|

PCI

at net national product at constant prices (in

Rupees) |

5352 |

7321 |

- |

16223 |

16910 |

17281 |

18517 |

19649 |

21005 |

|

Inflation

(WPI) (point-to-point) (1993-94=100)** |

16.7 |

12.7 |

4.4 |

5.5 |

1.6 |

6.5 |

4.6 |

5.1 |

4.1 |

|

Food

grains production |

18.1 |

3.1 |

-5.8 |

-6.2 |

8.1 |

-17.9 |

22.1 |

-4.2 |

2.3 |

Savings

and Investments

|

|

|

|

|

|

|

|

|

|

|

Gross

domestic savings |

21.2 |

24 |

25.1 |

23.5 |

23.6 |

26.5 |

28.9 |

29.1 |

- |

|

Gross

domestic investments |

22.7 |

27.4 |

26.9 |

24.2 |

23.0 |

25.3 |

27.2 |

30.1 |

- |

|

|

|

|

|

|

|

|

|

|

|

|

Sectoral

GDP # |

|

|

|

|

|

|

|

|

|

|

Agriculture,

forestry and fishing |

12.9 |

4.6 |

-0.9 |

0 |

6.2 |

-6.9 |

10 |

0.7 |

3.9 |

|

Industry |

3 |

6.3 |

11.6 |

6.3 |

2.7 |

7 |

7.6 |

8.6 |

8.7 |

|

Services |

4.3 |

4.4 |

10.5 |

5.6 |

7.1 |

7.3 |

8.2 |

9.9 |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

Social

Indicators |

|

|

|

|

|

|

|

|

|

|

Population

(in Million) |

679 |

839 |

- |

1019 |

1038 |

1055 |

1073 |

1090 |

|

|

Life

expectancy at birth (in years) |

50.4 |

58.7 |

- |

|

- |

- |

- |

- |

- |

|

Literacy

rate |

43.57 |

52.2 |

- |

65.38 |

- |

- |

- |

- |

- |

|

Note:*From

2000-01 the new series with base year 1999-00 |

|

|

|

|

|

|

|

||

|

**

Data for 1980-81 and 1990-91 relate to base year 1981-82) |

|

|

|

|

|

|

|

||

|

|

|||||||||

|

-'

implies data not available. |

|

|

|

|

|

|

|

|

|

|

Source:

Economic Survey, various issues |

|

|

|

|

|

|

|

|

|

The decadal GDP growth rates for 1980s (1980-81 to 1991-92) and 1990s (1992-93 to 2001-02) have worked out to 5.5 per cent and 6.1 per cent, respectively. Further, the economic growth rate has been hovering around 8 per cent since 2003-04. Similarly, per capita net national product (at 1993-94 prices) has risen from Rs 7,321 in 1990-91 to Rs 10,308 in 2000-01 and further to Rs 21,005 in 2005-06, showing a substantial increase in purchasing power in the hands of people. The savings and investment rates have also shown gradual increases except in the recessionary years of 2000-01 and 2001-02. The social indicators in terms of life expectancy and literacy rate, though they have not showed a very optimistic performance during the last few decades, albeit there has been some progress. Apparently, the Indian economy is on the high growth trajectory as exhibited by these broad macro economic indicators.

III

Empirical

Analysis for 1990s and Thereafter

Consumption

Expenditure

In

recent years, the relationship between income distribution and the

process of development has come increasingly come under scrutiny. As

mentioned above, there are no empirical evidences to establish firm

correlation between these two parameters given the problems associated

with the data availability. Yet, some indicators such as trends in

consumption expenditure by various sections of the society portray the

extent of income inequality in the country (Table 2). It is understood

that the prospect of declining income shares of the lower income groups

raises obvious questions about the welfare aspects of development.

Interestingly, the data released by UNDP disseminates revealing results,

which show that the share of consumption of the richest 10 and 20 per

cent to the poorest 10 and 20 per cent, respectively in

Table

2: Indicators of Income Inequality: Consumption Expenditure

|

||||||

|

|

|

|

||||

|

|

Survey

Period |

|||||

|

|

1997 |

1999-00 |

1996-2002 |

1998 |

2001 |

1996-2002 |

|

Share

of consumption |

|

|

|

|

|

|

|

Poorest

10 per cent |

3.5 |

3.9 |

- |

2.4 |

1.8 |

- |

|

Poorest

20 per cent |

8.1 |

8.9 |

8.9 |

5.9 |

4.7 |

4.7 |

|

Richest

20 per cent |

46.1 |

41.6 |

- |

46.6 |

50 |

- |

|

Richest

10 per cent |

33.5 |

27.4 |

- |

30.4 |

33.1 |

- |

|

Measures

of Inequality |

|

|

|

|

|

|

|

Richest

10 per cent to poorest 10 per cent |

9.5 |

7.0 |

- |

12.7 |

18.4 |

- |

|

Richest

20 per cent to poorest 20 per cent |

5.7 |

4.7 |

4.9 |

8 |

10.7 |

10.7 |

|

Gini

index * |

37.8 |

32.5 |

32.5 |

40.3 |

44.7 |

44.7 |

|

Notes:

* Measures inequality over the entire distribution of

consumption expenditure where a value of 0 and 100 represents

perfect equality and perfect inequality, respectively. |

||||||

|

Source:

UNDP, Human Development Report, various issues |

|

|

||||

Poverty

Another significant indicator of income distribution is the estimated of trends in poverty in terms of headcount ratio, that is, the proportion of population below poverty line (Table 3). Poverty trends in India have been a matter of intense controversy in the nineties as the extent of actual decline in the proportion of population below the poverty line between 1993-94 and 1999-2000 has been a subject of intense debate by academicians due to changes in the methodology for collection of basic data in 1999-2000 and possible non-comparability with earlier rounds of the consumer expenditure survey conducted by National Sample Survey Organisation (NSSO). In the absence of conclusive evidence, widely divergent claims have flourished. Some have argued that the nineties have been a period of unprecedented improvement in living standards. Other have claimed that it has been a time of wide spread impoverishment. Clearly, as per the Planning Commission, the headcount ratio has declined significantly from 1980s to 1990s and further in 2000. The broad picture shows that there has been a sustained decline in poverty in most of the states during the reference period.

|

Table

3: Poverty Estimation: State-wise

Headcount Ratio |

||||||||

|

|

1983 |

1987-88 |

1993-94 |

1999-00 |

Adjusted

poverty |

|||

|

State/Uts |

|

|

|

Rural |

Urban |

Combined |

Ratios: |

|

|

|

|

|

|

|

|

|

55

th Round |

|

|

|

|

|

|

|

|

|

(1999-2000) |

|

|

|

|

|

|

|

|

|

Rural |

Urban |

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

(9) |

|

All

|

44.48 |

38.86 |

35.97 |

27.09 |

23.62 |

26.10 |

30.2 |

24.7 |

|

Andhra

Pradesh |

28.91 |

25.86 |

22.19 |

11.05 |

26.63 |

15.77 |

14.9 |

27.7 |

|

Arunachal

Pradesh |

40.88 |

36.22 |

39.35 |

40.04 |

7.47 |

33.47 |

- |

- |

|

|

40.47 |

36.21 |

40.86 |

40.04 |

7.47 |

36.09 |

44.1 |

8.3 |

|

|

62.22 |

52.13 |

54.96 |

44.30 |

32.91 |

42.60 |

49.2 |

33.8 |

|

|

18.90 |

24.52 |

14.92 |

1.35 |

7.52 |

4.40 |

|

|

|

|

32.79 |

31.54 |

24.21 |

13.17 |

15.59 |

14.07 |

15.4 |

16.0 |

|

Haryana |

21.37 |

16.64 |

25.05 |

8.27 |

9.99 |

8.74 |

12.7 |

9.5 |

|

Himachal

Pradesh |

16.40 |

15.45 |

28.44 |

7.94 |

4.63 |

7.63 |

18.9 |

4.5 |

|

|

24.24 |

23.82 |

25.17 |

3.97 |

1.98 |

3.48 |

|

|

|

Karnataka |

38.24 |

37.53 |

33.16 |

17.38 |

25.25 |

20.04 |

25.7 |

25.5 |

|

Kerala |

40.42 |

31.79 |

25.43 |

9.38 |

20.27 |

12.72 |

12.6 |

18.7 |

|

Madhya

Pradesh |

49.78 |

43.07 |

42.52 |

37.06 |

38.44 |

37.43 |

36.4 |

37.9 |

|

|

43.44 |

40.41 |

36.86 |

23.72 |

26.81 |

25.02 |

29.2 |

28.1 |

|

Manipur |

37.02 |

31.35 |

33.78 |

40.04 |

7.47 |

28.54 |

- |

- |

|

Meghalaya |

38.81 |

33.92 |

37.92 |

40.04 |

7.47 |

33.87 |

- |

- |

|

Mizoram |

36.00 |

27.52 |

25.66 |

40.04 |

7.47 |

19.47 |

- |

- |

|

Nagaland |

39.25 |

34.43 |

37.92 |

40.04 |

7.47 |

32.67 |

- |

- |

|

Orissa |

65.29 |

55.58 |

48.56 |

48.01 |

42.83 |

47.15 |

47.3 |

41.4 |

|

|

16.18 |

13.20 |

11.77 |

6.35 |

5.75 |

6.12 |

5.9 |

6.3 |

|

Rajasthan |

34.46 |

35.15 |

27.41 |

13.74 |

19.85 |

15.28 |

19.6 |

22.8 |

|

|

39.71 |

36.06 |

41.43 |

40.04 |

7.47 |

36.55 |

|

|

|

Tamil

Nadu |

51.66 |

43.39 |

35.03 |

20.55 |

22.11 |

21.12 |

19.9 |

24.4 |

|

Tripura |

40.03 |

35.23 |

39.01 |

40.04 |

7.47 |

34.44 |

- |

- |

|

Uttar

Pradesh |

47.07 |

41.46 |

40.85 |

31.22 |

30.89 |

31.15 |

33.7 |

30.4 |

|

|

54.85 |

44.72 |

35.66 |

31.85 |

14.86 |

27.02 |

37.1 |

19.5 |

|

Andaman

& Nicobar |

52.13 |

43.89 |

34.47 |

20.55 |

22.11 |

20.99 |

- |

- |

|

|

23.79 |

14.67 |

11.35 |

5.75 |

5.75 |

5.75 |

- |

- |

|

Dadra

& Nagar Haveli |

15.67 |

67.11 |

50.84 |

17.57 |

13.52 |

17.14 |

- |

- |

|

|

26.22 |

12.41 |

14.69 |

0.40 |

9.42 |

8.23 |

- |

0.7 |

|

|

42.36 |

34.95 |

25.04 |

9.38 |

20.27 |

15.60 |

- |

- |

|

|

50.06 |

41.46 |

37.40 |

20.55 |

22.11 |

21.67 |

- |

- |

|

Source:

Planning Commission

(2002): National Human

Development Report, 2001, March. |

|

|||||||

However,

wide variations have been noticed in the poverty ratios of different

states. The ratio for Orissa at 47.15 per cent is about eight times that

for

Employment

The changes in the pattern of employment structure have a significant impact on varying degrees of income inequality. Since the governments function within the administrative and fiscal constraints, the target group programmes normally have a marginal impact on income redistribution. Other economic instruments such as target group policies and programmes have a short-term impact, but the income redistribution through employment is generally viewed as more sustainable.

Current Employment and Unemployment Scenario

It is essential to focus on broad employment situation as it exists today, which indicates the extent and direction of income inequalities across all sections of the society. Some such aspects are listed below:

- 7.32 per cent of the labour force in 1999-2000 was unemployed. In absolute terms the number of unemployed stood at 26.58 million.

- Since the above estimates are on Current Daily Status basis, the number of unemployed also includes the number of those who are underemployed in terms of underutilization of the labour time. But it excludes such underemployed who are working at very low levels of income and productivity.

- Among the employed, the proportion of poor is as high as in the population at large, suggesting a large proportion of workers engaged in subsistence employment.

- Only about 8 per cent of the total employment is in organised sector leaving more than 90 per cent engaged in informal sector activities, which is, largely outside the reach of any social security benefits.

- The educational and skill profile of the large proportion of the existing workforce is very poor.

Current

State of

Labour

Force Skills

It

is not easy to quantify the level of skills in the labour force because

these data sets are not readily available. What is available is

information on the education attained by the labour force. About 44 per

cent of all workers in 1999-2000 were illiterate and another 22.7 per

cent had schooling only up to the primary level. If we define the

minimum level of education necessary to function in a modern economy as

schooling up to the middle level, then only about 33.2 per cent of the

labour force had schooling of that level and above. The percentage was

higher at 57.4 per cent for the urban labour force, but it was

correspondingly worse in rural areas, with only 25.4 per cent for the

rural labour force meeting these standards. This, undoubtedly,

provides enough support for a high incidence of rural-urban income

disparities based on positive education–income correlation. It is

largely evident that education levels in the labour force in

Moreover,

the levels of vocational skills in the Indian labour force compares

poorly with the position in other countries. Only 5 per cent of the

Indian labour force in the age group of 20-24 is trained in vocational

skills whereas the same in industrial countries is much higher, varying

between 60-80 per cent. In the long term, a strategy to impart

vocational skills will facilitate increase in income of labour through

changes in their occupational profile at a rapid pace. This is because

the traditional avenues for work in agriculture are poised to alter

substantially, as ability of this sector to absorb the work force has

diminished at a fast pace over the last two decades. Therefore, a

greater emphasis on vocational training in relation to general education

is required.

Income

Inequalities arising out of Structural Adjustments in Employment Pattern

|

Table

4 : Growth in Employment during 1993-94 and 1999-2000 |

||

|

Sector |

Per

cent change per annum in employment growth (1999-2000/1993-97) |

|

|

|

|

|

|

|

UPSS

# |

CDS* |

|

Agriculture |

-0.34 |

-0.12 |

|

Mining

and Quarrying |

-2.85 |

-2.55 |

|

|

|

|

|

Manufacturing |

2.05 |

2.66 |

|

Electricity,

gas and water supply |

-0.88 |

-3.43 |

|

Construction |

7.09 |

5.22 |

|

|

|

|

|

Trade,

hotels and restaurants |

5.04 |

5.85 |

|

Transport

storage and communication |

6.04 |

5.61 |

|

Finance,

insurance, real estate and business services |

6.2 |

5.62 |

|

Community,

social and personal services |

0.55 |

-2.0 |

|

|

|

|

|

All-India

Work force |

0.98 |

1.07 |

|

All-India

Labour force |

1.07 |

1.31 |

|

Unemployment

rate (per cent) 1999-00 |

2.2 |

7.32 |

|

Notes:

# Usual Principal Subsidiary Status based on old population Census

and Technical Group *Usual

Daily status based on 2001 Population Census Source:

Planning Commission (2002): Report of Special Group on

Targeting Ten million Employment Opportunities a Year in Tenth

Plan |

||

Agricultural Wages

Though, the share of agriculture in the total employment as reflected by an absolute fall in agricultural employment during 1993-94 to 1999-00 (Table 4) has been declining over the years, the pace of this deceleration has been slower than the pace of shrinking share of agriculture in the GDP. As a result, a clear divergence has emerged between the shares of primary, secondary and tertiary sectors in employment and output, suggesting thereby large inter-sectoral differences in the per worker incomes. In this context, trends in agricultural wages prove to be an important indicator reflecting increasing preference of the labour force to shift towards non-agricultural activities. According to ‘Agricultural Wages in India’, published by the Directorate of Economics and Statistics, Ministry of Agriculture, the real agricultural wages grew at 5 per cent per annum in 1980s and 2.5 per cent per year in the 1990s. Interestingly, with the introduction of the Fifth Pay Commission by the central as well as the state governments, salaries in the public sector during the 1990s have grown at almost 5 per cent per year. Given that salaries of public sector employees tend to be much better of than agricultural labourers, this can be taken as an instance of rising economic disparities between different occupation groups. Since agricultural labourers and public sector employees typically reside in rural and urban areas, respectively, this finding may just be another side of the coin of rising rural-urban disparities. Moreover, for the medium and high skill-based workers, with the emergence of newer industries like BPOs and call centres catering to foreign clients, especially in the fields of information technology (IT), Information Technology Enabled Services (ITES), banking and finance, the income levels in these areas have risen disproportionately in a short span leaving large sections of the society with marginal or negligible wage increases over the last decade, thereby contributing to increasing income inequalities.

After

reviewing the broad indicators of emerging income inequalities, it might

be argued that a short-term increase in income inequality is to be

expected in a liberalising economy. However, China’s experience (Table

2) of sharp and sustained increase in economic inequality over a period

of more than 20 years, after market-oriented reforms were initiated in

the late 1970s, does not inspire much confidence in this prognosis. It

is in fact, an important pointer to the possibility of a further

accentuation of economic disparities in

IV

Instances of Increasing Income Disparities

Slum

Population

Interestingly, although poverty levels have come down in most of the states from 1993-94 to 1999-00, the poor population has been increasingly shifted towards urban areas in search of jobs resulting in ever-increasing slum population in urban areas in most of the states (Table 5). One of the glaring facts underlined by the rising proportion of slum population to urban population (from 21 per cent in 1991 to 28 per cent in 2001 at all India level) essentially shows increasing concentration of poor in urban areas and underlines the glaring fact of either underdevelopment or a very slow pace of growth in other backward regions. As expected, this phenomenon has been more prominent through 1990s in most states.

|

Table 5: State-wise Urban Slums

in |

|||||||||||||

|

States |

Urabn

Population (lakh) |

Percent

Change |

Slum

Population |

Percent

Change |

Slum

Population as per cent |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

of

Urban Population |

|

|

|

|

2001 |

1991 |

1981 |

2001/1991 |

1991/1981 |

2001 |

1991 |

1981 |

2001/1991 |

1991/1981 |

2001 |

1991 |

1981 |

|

Andhra Pradesh |

249.7 |

178.9 |

124.9 |

39.6 |

43.2 |

60.2 |

43.1 |

28.6 |

39.5 |

50.9 |

24.1 |

24.1 |

22.9 |

|

Arunachal Pradesh |

1.9 |

1.1 |

0.4 |

69.9 |

167.1 |

0.4 |

0.2 |

0.0 |

69.7 |

- |

20.0 |

20.0 |

0.0 |

|

|

32.4 |

24.9 |

17.8 |

30.1 |

39.6 |

5.8 |

4.5 |

1.2 |

30.0 |

262.7 |

18.0 |

18.0 |

7.0 |

|

|

149.6 |

113.5 |

87.2 |

31.7 |

30.2 |

35.4 |

26.9 |

32.7 |

31.7 |

-17.7 |

23.7 |

23.7 |

37.5 |

|

Chattisgarh |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

|

|

6.6 |

4.8 |

3.5 |

36.7 |

36.4 |

1.1 |

0.8 |

0.2 |

37.0 |

244.2 |

17.4 |

17.4 |

6.9 |

|

|

190.0 |

142.5 |

106.0 |

33.4 |

34.4 |

34.4 |

25.8 |

15.3 |

33.2 |

68.5 |

18.1 |

18.1 |

14.4 |

|

Haryana |

59.6 |

40.6 |

28.3 |

46.9 |

43.4 |

10.1 |

6.8 |

2.7 |

47.1 |

149.6 |

16.9 |

16.9 |

9.7 |

|

Himachal Pradesh |

5.8 |

4.5 |

3.3 |

28.3 |

37.8 |

1.6 |

1.3 |

0.8 |

28.7 |

64.8 |

28.0 |

27.9 |

23.3 |

|

|

24.2 |

18.4 |

12.6 |

31.4 |

45.9 |

7.8 |

5.9 |

6.3 |

31.4 |

-5.6 |

32.2 |

32.2 |

49.7 |

|

Jharkhand |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

|

Karnataka |

191.0 |

139.1 |

107.3 |

37.3 |

29.6 |

17.8 |

12.9 |

5.8 |

37.3 |

125.1 |

9.3 |

9.3 |

5.4 |

|

Kerala |

103.5 |

76.8 |

47.7 |

34.7 |

61.0 |

16.5 |

12.2 |

4.1 |

34.7 |

197.9 |

15.9 |

15.9 |

8.6 |

|

Madhya Pradesh |

204.1 |

153.4 |

105.9 |

33.0 |

44.9 |

28.0 |

21.0 |

10.8 |

32.9 |

95.6 |

13.7 |

13.7 |

10.2 |

|

|

416.2 |

305.4 |

219.9 |

36.3 |

38.9 |

107.4 |

78.7 |

43.2 |

36.4 |

82.4 |

25.8 |

25.8 |

19.6 |

|

Manipur |

6.7 |

5.1 |

3.8 |

32.6 |

34.6 |

1.1 |

0.9 |

0.2 |

32.7 |

417.0 |

16.9 |

16.9 |

4.5 |

|

Meghalaya |

4.6 |

3.3 |

2.4 |

39.6 |

36.8 |

1.2 |

0.8 |

0.7 |

39.8 |

26.2 |

25.2 |

25.2 |

27.4 |

|

Mizoram |

6.4 |

3.2 |

1.2 |

102.1 |

161.0 |

1.2 |

0.6 |

0.0 |

102.1 |

- |

18.1 |

17.9 |

0.0 |

|

Nagaland |

3.1 |

2.1 |

1.2 |

46.4 |

73.2 |

0.6 |

0.4 |

0.0 |

46.4 |

- |

20.0 |

20.0 |

0.0 |

|

Orissa |

56.3 |

42.4 |

31.1 |

33.0 |

36.2 |

11.2 |

8.4 |

2.8 |

32.9 |

199.0 |

19.9 |

19.9 |

9.1 |

|

|

80.2 |

59.9 |

46.5 |

33.9 |

28.9 |

18.9 |

14.1 |

11.7 |

33.9 |

21.2 |

23.6 |

23.6 |

25.1 |

|

Rajasthan |

137.2 |

100.7 |

72.1 |

36.3 |

39.6 |

32.7 |

24.0 |

10.3 |

36.0 |

134.1 |

23.8 |

23.8 |

14.2 |

|

|

0.5 |

0.4 |

0.5 |

29.7 |

-27.6 |

0.1 |

0.1 |

0.0 |

29.5 |

295.8 |

25.7 |

25.7 |

4.7 |

|

Tamil Nadu |

233.1 |

190.8 |

159.5 |

22.2 |

19.6 |

43.6 |

35.7 |

26.8 |

22.0 |

33.5 |

18.7 |

18.7 |

16.8 |

|

Tripura |

5.1 |

4.2 |

2.3 |

20.4 |

86.9 |

0.9 |

0.7 |

0.2 |

20.0 |

304.3 |

17.6 |

17.6 |

8.2 |

|

Uttar Pradesh |

365.4 |

276.1 |

198.9 |

32.4 |

38.8 |

77.1 |

58.4 |

25.8 |

32.0 |

126.3 |

21.1 |

21.2 |

13.0 |

|

Uttranchal |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

na |

|

|

236.6 |

187.1 |

144.5 |

26.5 |

29.5 |

65.8 |

52.0 |

30.3 |

26.6 |

71.6 |

27.8 |

27.8 |

21.0 |

|

All States |

2769.4 |

2078.8 |

1528.8 |

33.2 |

36.0 |

580.7 |

436.5 |

260.2 |

33.0 |

67.7 |

21.0 |

21.0 |

17.0 |

|

UTS |

140.1 |

92.3 |

65.8 |

51.8 |

40.2 |

37.6 |

26.2 |

18.9 |

43.8 |

38.0 |

26.8 |

28.3 |

28.8 |

|

|

122.9 |

84.7 |

57.7 |

45.1 |

46.9 |

32.6 |

22.5 |

18.0 |

44.9 |

24.9 |

26.5 |

26.5 |

31.2 |

|

|

2209.4 |

2176.1 |

1594.6 |

33.7 |

36.5 |

618.3 |

462.7 |

279.1 |

33.6 |

65.8 |

28.0 |

21.3 |

17.5 |

|

na:

Not available or not relevant Source:

NSUS : National Slum Upgradation Scheme |

|||||||||||||

Inter-state

Differences

The overall disparity in inter-state growth of net state domestic product (NSDP) and per capita NSDP of states has increased considerably during the nineties as compared to the eighties and the seventies. (Table 6). In recent times, the decade of 1980s seems to be a period in which horizontal inequity across states was lower than that compared with the 1990s where the magnitude of disparities has been maximum.

|

Table

6:Disparity in Growth amongst States/Union Territories |

||||

|

Period |

Measure

of disparity in

Growth

Standard

deviation |

Relative

measure of disparity in growth between per capita income and

NSDP (Covariance) |

||

|

NSDP |

Per

capita NSDP |

|||

|

1970-71

to 1979-80 |

2.22 |

1.81 1.02 2.4 |

3.67 |

|

|

1980-81

to 1990-91 |

1.71 |

0.71 |

||

|

1993-94

to 1998-99 |

3.13 |

5.23 |

||

|

Note:

The higher the value, the more the disparity. |

||||

|

Source:

Central Statistical Organsiation |

||||

A comparison of the trends in rates of economic growth for all the states in the 1990s shows that less developed regions including the north eastern states, Orissa and the heartland states of Bihar, Uttar Pradesh and Madhya Pradesh have generally recorded growth rates below the all- India average during the most recent period of 1993-94 to 1998-1999. This trend suggests a widening of the gap between the more and the less developed states.

Income

Tax

The data on income tax paid, number of returns filed and income of those who have filed the returns (Appendix A) show that there has been a shift in the levels of income with increasing higher levels of income. There has been a significant shift in the income levels during the period 1990-91 to 1999-00. In the slab 50,001-1,00,000, the number of returns filed which stood at 17 per cent of the total returns filed in 1990-91 increased to 37 per cent and 63 per cent in 1993-94 and 1990-00, respectively. Similarly, income from returns as a per cent of total income at 28 per cent in 1990-91 has risen to 44 per cent in 1999-2000 for this income slab. Those earning over 10 lakhs annually as a per cent of total number of returns have increased from 0.04 per cent in 1990-91 to 0.55 per cent in 1999-2000. But more importantly, their share in total tax paid has increased from 6 per cent to 24 per cent during the same period. This indicates the rising share of income of those earning above 10 lakhs while those earning between Rs 50,000 to Rs 1,00,000 has reduced from 34 per cent in 1990-91 to 13 per cent in 1999-00.

Summing

up

Despite an optimistic macro-economic scene (as reflected in Table 1) and reducing poverty (as depicted in Table 3), there is a fundamental inquiry raised as to what extent the overall economic growth has been meaningful to masses or broad sections of the society. Clearly, there are indications of increasing income disparities in the country. There is no full proof redistrbutive mechanism or instant solution to tackle this problem. However, in the long run, we need some strategy to narrow down widening income gaps across the wide spectrum of the society so as to attain a permissible level of income disparities, which, in fact, could be conducive to growth. For the present, there is a need for the government to play more active role in providing social security safety net as well as for the private sector to assume a greater responsibility given their pivotal role being played in the economy.

Annexure

A

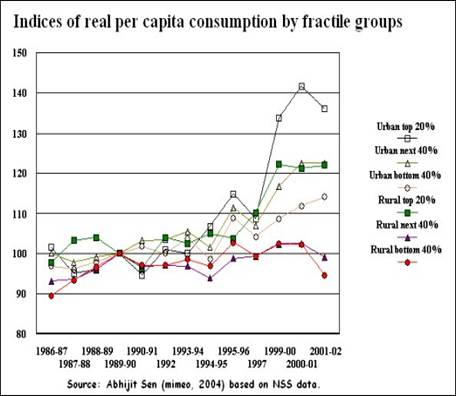

In the article titled ‘Poverty and Inequality in India –II, Widening Disparities during the 1990s’ Abhijit Sen and Himanshu, have depicted sharp increases in income inequalities in the 1990s in all respects and have concluded that poverty reduction has deteriorated markedly despite higher growth during the reference period. The chart below shows some very clear trends in terms of which sections of the population have benefited and which have lost out during the years of economic reforms.

The

most dramatic and remarkable improvement in consumption has been for

those who were already the richest people in

This is the

highest and most rapid increase in the consumption of the rich that has

ever been recorded in

By

contrast, the bottom 40 per cent of the urban population relatively

little increase in per capita consumption compared to these other

groups, at only around 14 per cent since 1989-90. But the most

dramatic evidence is for the bottom 80 per cent of the rural

population – well more than half of

References:

Planning Commission, Tenth Five-Year Plan Documents (2002-07), Volume III

UNDP, Human Development Report, various issues

Deaton,

Angus and Jean Dreze (2002): ‘Poverty and Inequality in

Sen

Abhijit and Himanshu (2004): ‘Poverty and Inequality in

Widening Disparities during the 1990s’, Economic and Political Weekly, September

---------------------------------------------------------------------------------------------------

*This note is prepared by Ms Piyusha Hukeri and Ms Gauri Ranade.

![]()

Highlights of Current Economic Scene

AGRICULTURE

The central government has announced a further increase of Rs 40 per quintal, in addition to the previously announced Rs 10 per quintal rise, in the minimum support price (MSP) of paddy for the ensuing 2006-07 kharif marketing season. With the latest modification, the MSP has been raised to Rs 620 for common paddy and Rs 650 per quintal for ‘Grade A’ varieties from Rs 580 per quintal and Rs 610 per quintal, respectively.

The central government has re-imposed various controls, including stock holding limits on wheat and pulses trade, to keep the prices of these two commodities under control. The restriction would be applicable for 6 months, with no limitations on inter-state movements or imports.

The Minerals and Metals Trading Corporation (MMTC) Ltd., a state-owned trading company, has cancelled a tender to buy1.2 lakh tonnes of wheat due to high tender price. The corporation had floated the tender on August 8, 2006, in response to which, Germany-based AC Toefer had offered to supply about 1.25 lakh tonnes wheat at a price ranging from $219-227 per tonne, on cost and freight (C&F) basis.

The

performance audit of foodgrain management by the Comptroller and Auditor

General (CAG) of India has revealed significant inefficiencies in grain

procurement that have cost the country about Rs 1,310.3 crore between

2000-01 and 2004-05. The report has indicated diversion of over 4.4

million tonnes of foodgrains meant for the targeted public distribution

system (TPDS) in 10 states, including

The

central government has allowed import of an additional 20-lakh tonnes of

wheat at zero custom duty as a part of measures to meet the shortfall in

procurement for Public Distribution System (PDS). State –run food

corporation of

As per the Central Silk Board, silk export earnings of the country have exceeded the target (Rs 2,800 crore) set for the fiscal year 2005-06, on account of higher demand for readymade silk garments in the global market. Export earnings have surged by 9.7 per cent to Rs 3158.2 crore from Rs 2,879.6 crore during last fiscal year. The US, UK, Italy, German Republic and Spain have emerged as the top 5 countries importing Indian silk goods, accounting for 58.1 per cent of the total export earnings.

Southern

Shrimp Alliance (SSA), an organisation of shrimp farmers based in the

The government of Andhra Pradesh has plans to undertake the cultivation of bio-diesel plants like Pongamia and Jatropa on at least 1 lakh acre of land in each in 13 districts under the National Rural Employment Guarantee Programme (NREGP). Apart from providing financial support to the tune of Rs 3,500 per acre, to farmers interested in bio-diesel plantation, the government would also create marketing facilities for bio-diesel produced under the scheme.

The government of Karnataka and Agriculture and Processed Food Products Export Development Authority (APEDA) has plans to set up an agri export zone (AEZ) for Vanilla, entailing an investment of Rs 2.56 crore. APEDA would assist the state government in supplying quality planting material, plant protection and post harvest handling, training on vanilla cultivation, micro irrigation, processing units, in setting up quality control labs and imparting organic farming techniques. Six districts, namely, Dakshina Kannada, Uttara Kannada, Udupi, Shimoga, Kodagu and Chickamagalur have been selected for the AEZ.

Infrastructure

Power

Independent power producers (IPPs) like Sterlite, Essar Power, Tata Power Company, etc, with investments planned in various states, have sought the power ministry’s intervention for an early decision on long term coal linkages for their upcoming projects arguing that a delayed decision would stall the financial closure and in turn delay the project development.

The synchronisation of the country's largest and most power-deficit grid – the northern grid – with the eastern, north-eastern and western grids will be achieved from September. The attempt to synchronise operations in four of the country's five regional grids was prompted by a need to ramp up the interconnection between the northern and eastern grids for transferring up to 1,000 MW surplus power from the eastern region to the energy-deficit northern region. With the prospect of the four regions operating together in synchronisation, apprehensions of any potential grid indiscipline endangering the grid security in all the four regions have prompted the grid managers to stipulate measures such as a blanket ban on bypassing of under frequency relays (UFRs) in the regions.

The non-availability of gas is forcing producers to run power projects below capacity while investors are being forced to shelve upcoming projects. For example, the petroleum ministry has recently turned down Reliance Energy Ltd’s (REL) plea for conversion of 0.36 metric million standard cubic meters per day (mmscmd) fall back allocation of natural gas as firm allocation for its Samalkot Combined Cycle Power Station in Andhra Pradesh stating shortage of gas supply in the region and no possibility for any new allocation of natural gas or converting the fall back allocation into firm allocation at present. Similarly, the non-availability of gas has forced West Bengal Power Development Corporation Ltd (WBPDCL) to shelve gas-fired component of 2,000 mw combined cycle power project power project and the corporation has failed to tie up the required gas supply for the project.

Petroleum,

Petroleum Products and Natural Gas

The country's crude oil production has risen by 4.1 per cent in July 2006 to 2.87 million tonnes (mt) from 2.75 mt during the corresponding month last year. The country's natural gas output has risen by 2.4 per cent to 2.76 billion cubic meters (bcm) in the month under review from 2.69 bcm during the same period last year.

Non-Conventional

Energy

The Andhra Pradesh government has announced plans to take up cultivation of bio-diesel plants in 13 districts under the National Rural Employment Guarantee Programme (NREGP). The chief minister has also expressed interest in providing financial support to the tune of Rs 3,500 per acre to farmers interested in bio-diesel plantation. The state government has proposed to venture into the plantation of pongamia and jatropa on at least 1 lakh acre of land in each of the 13 districts under the NREGP programme during 2006 and to further create marketing facilities for bio-diesel produced under the scheme.

A 3.5 MW capacity power project using poultry droppings as fuel will go on stream in Tamil Nadu's Tiruchengodu taluk on August 26, 2006. The project has been developed under the demonstration category of power projects under the ministry of non-conventional energy Sources (MNES) and is being promoted by the Tiruchengodu-based Subhashri Bio Energies Pvt Ltd at a cost of Rs 40 crore. It has been granted Rs 6 crore from the MNES and a term loan of Rs 14 crore from Indian Overseas Bank. Besides the promoters' contribution of Rs 6 crore, the project has also been given working capital to the tune of Rs 14 crore. Originally planned as a 2-MW power project, the generation capacity has been enhanced to 3.5 MW; the plant is fed with 325 tonnes of poultry litters every day to generate power. It is also equipped to produce 150 tonnes of manure as a by-product daily from the slurry generated out of the plants digestors after generating power. The location has been chosen considering the density of poultry farms in the vicinity as the contiguous Namakkal poultry tract with three crore birds generating over 1,500 tonnes of poultry litters every day. Subhashri Bio Energies has already entered into a power purchase agreement with the Tamil Nadu Electricity Board which would be buying the energy generated from the plant at Rs 3.15 per unit.

Steel

The

steel ambitions of the three iron ore rich states of Orissa, Jharkhand and

Chhattisgarh have moved far beyond the 100 million tonnes annual steel

making capacity by 2019-20 envisaged in the National Steel Policy approved

by the government in November 2005. In fact, going by the list of probable

steel producing units lined up by these three states,

Coal

The

reform process in the domestic coal mining sector is set to gain further

momentum with a series of new coal projects being planned to be developed

by Coal India Ltd (CIL) by outsourcing nearly all mine preparation and

coal extraction jobs to leading international and domestic companies in

the coming months. CIL has been allowed to start developing at least nine

large coal projects as early as possible so that it can achieve the

targeted production by 2011-12. In fact, these are part of a total 13

large projects, each costing more than Rs 100 crore, which have been

approved by the union coal ministry, while 10 more large projects are

expected to get approval shortly. In almost all the projects, jobs such as

overburden removal and coal extraction will be outsourced from private

operators, except in two where either the overburden removal or coal

extraction only will be done privately. Meanwhile, the Central Mine

Planning & Design Institute has prepared a total of 97 detailed

project reports for CIL, which may be developed in the Tenth and Eleventh

Plan periods. Of the total projects, some 23 large ones each with an

investment of over Rs 100 crore have been placed before the ministry for

approval. A total of 25 projects with an investment of less than Rs 100

crore were placed before the CIL board and the balance 49 projects each

with an investment of about Rs 50 crore were to be approved by the

respective subsidiary of CIL. The board has approved 19 projects while the

subsidiaries have cleared a total of 41 projects so far.

Roads

The

ministry of road transport and highways has circulated cabinet notes

regarding projects in the NHDP phases V (8 projects) and VI (1 project).

The phase V envisages six-laning of existing four lane highways; work on

one section, Vadodara to

Railways

The Indian railways has set goals for obtaining a larger share of the freight traffic; a part of its objectives for the 11th Plan is to target particular commodities such as cement, iron and steel and containerised traffic and resultantly triple its share in transporting them. In 2005, the railways carried 55 mt of cement, which it plans to increase to 200 mt by 2010 by tapping not only finished cement but also related raw materials like clinker, fly ash, coal, limestone, dolomite and gypsum. The railways also has plans to increase its freight carrying in iron and steel to 200 mt as against the 83 mt in 2005 as well as increase its freight in the containerised traffic segment from the current 18 mt to 100 mt by 2010. As part of these efforts, the railway ministry is planning to sign long-term service agreements with players in these sectors; the agreements would be for a period of 5-10 years and entail fines in case of delays by either party. Under the 11th Plan, the railways will also embark on a new wave of expansion of infrastructure, which would include construction of unloading terminals, warehouses, covered sheds and specialised wagons. The ministry has also decided not to ask for any funds under the 11th Plan wanting to carry out all these projects through internally generated funds and private investments or possibly third party logistics.

Inflation

The annual point-to-point inflation rate based on wholesale price index (WPI) has gone up to 4.92 per cent for the week ended August 12, 2006 from 4.82 per cent during the previous week. The inflation rate was at 3.67 per cent in the corresponding week last year.

The WPI in the week under review has gone up by 0.2 per cent to 204.7 from the previous weeks’ level of 204.3 (Base: 1993-94=100). The index of ‘primary articles’ group (weight 22.02 per cent) has increased by 0.5 per cent to 203.6 from its previous week’s level of 202.5, mainly due to an increase of 0.5 per cent in the price index of both, the ‘food articles’ and ‘non-food articles’. The index of ‘food articles’ has gone up to 204.8 from 203.7 in the previous week, mainly due to the higher prices of fruits and vegetables and condiments and spices. Similarly, the index of ‘non-food articles’ has increased to 184.7 from 183.8, mainly due to the higher prices of raw rubber, raw cotton, niger seed and groundnut seed. The index of ‘fuel, power, light and lubricants’ group (weight 14.23 per cent) has remained unchanged at its previous week’s level of 328.4. The index of ‘manufactured products’ group constituting the maximum of 63.7 per cent of total weight, has risen a tad by 0.1 to 177.4 from the previous weeks’ level of 177.2, mainly due to the higher prices of textiles, base metals,’ ‘non-metallic mineral products’ and ‘transport equipment and parts’.

The latest final index of WPI for the week ended June 17, 2006 has been revised upwards; as a result both, the absolute index and the implied inflation rate stood at 203.5 and 5.50 per cent as against their provisional levels of 203.4 and 5.44 per cent, respectively.

Public

Finance

The tax revenue of VAT (Value Added Tax) implementing states has seen an increase of 27.1 per cent for the first quarter of the fiscal year 2006-07 over the corresponding period of the previous year. The tax revenue of theses states has displayed a growth of 13.8 per cent for the year 2005-06 over the previous year. This growth has been higher than the compound annual growth rate of sales tax revenues of these states for last five years.

The Empowered Committee of state finance ministers on VAT and Finance Ministry have finalised a compensation package for phasing out the Central Sales Tax (CST). States also have informed the Central government that they would be willing to consider 40 per cent share of the overall service tax proceed instead of 50 per cent demanded earlier, as an interim compensation measure. They have also abandoned their demand to include sugar, tobacco and textiles under VAT and have instead suggested continuing with the present norm of the Centre allocating one per cent from its revenue collection to the states towards these three items. The states have projected an 18 per cent CST growth and have accordingly pointed out that the losses on account of reduction in CST from 4 to 3 per cent from October 1, 2006 would be Rs 2,500 crore this fiscal and Rs 12,000 crore next fiscal.

The Finance Ministry has set a target of indirect tax arrears recovery at Rs 2,450 crore for 2006-07. Of this target, the Central Board of Excise and Customs (CBEC) has been expected to recover Rs 650 crore as customs duty, Rs 1,300 crore as central excise duty and Rs 500 crore as service tax arrears. As on February 28, 2006, the pending recovery of total indirect tax arrears has stood at Rs 21,578 crore. Out of this amount, Rs 7,533 crore has been stayed by various courts and hence was not recoverable.

Direct

tax collection from the Mumbai zone has recorded a huge increase of 137.5

per cent to Rs 11,400 crore during the period April 1, 2006 to July 15,

2006 as compared to Rs 4,800 crore for the corresponding period of the

previous year. This healthy growth reflects strong performance of industry

sectors such as banking, automobile, pharmaceuticals and insurance. The

target collection from the Mumbai zone for the entire financial year

2006-07 is Rs 69,000 crore.

The

finance ministry has been preparing a paper on the rationalisation of

non-merit subsidies as part of a larger expenditure management plan. It

has been expected to finish the preparation within three months. The next

budget may refurbish the subsidy structure.

The

Delhi Bench of the Income-Tax Appellate Tribunal has reached on a verdict

that there would be no tax liability for downlinking services of satellite

companies based in countries that have a Double Taxation Avoidance

Agreement (DTAA) with

Banking

In

a move to speed up financial inclusion in the north-east (NE) region, the

RBI has recommended the commercial banks to prepare a roadmap so that the

branches in this region can give banking access to 50 new households every

month for the next four years with a deposit account, with option to the

household of opening such account as a “no frills” account. A

committee of the central bank which was chaired by deputy governor Usha

Thorat has held extensive discussions with different stakeholders in all

the seven states of the region and said that the focus should be on

proactively connecting banks to the people, rather than waiting for

walk-in-customers. Taking into account the balances maintained in such

accounts over a period, the bank may offer small overdrafts or general

credit credit cards against such accounts and other products. The apex

bank has also recommended setting-up of a dedicated SME Debt Fund by SIDBI,

in association with major banks, to provide-finance upto 25 per cent of

project cost to first time entrepreneurs investing in agro-processing,

agro-based industries and SME sector, where a bank is willing to provide

the required funds. It has also suggested enhancement of insurance cover

under Credit Guarantee Fund Trust for Small Scale Industries (CGTSI)

scheme to cover up to 90 per cent in the NE region, as against the risk

cover of 75 per cent subject to a maximum of Rs 25 lakh available in the

rest of the country.

The

Bangalore-based Syndicate Bank has revised its benchmark primary lending

rate (BPLR) from 11.25 per cent to 11.50 per cent with effect from August

23, 2006.

Financial Markets

Capital

Markets

Primary Market

Action

Construction Equipment Ltd is to tap the market between September 1 and 7

through issue of shares of Rs 10 each in a price band of Rs 110 and Rs 130

per equity share.

Secondary

Market

The stock market has remained bullish with the BSE sensex registering a gain of 107 points to close the week at 11572.20 as the international crude oil prices eased. Moreover, the banks extended their recovery on expectations that interest rates may not rise in the near term. The state bank of India (SBI) has received an additional boost after the Union Cabinet paved the way for a follow-on public issue by approving the SBI (Amendment) Bill. The bill proposes to lower the floor for RBI’s holding in SBI to 51 per cent from 59.73 per cent held currently. Meanwhile, the bank’s board has ratified the bank’s decision early this month to raise prime lending rate by 25 basis points.

Among

the sectoral indices of BSE, barring capital goods, FMCG and health care

indices, all the others have registered positive gains with the highest

gain being recorded by metal index of about 4 per cent. While BSE sensex

recorded a rise of 0.9 per cent so did the BSE mid-cap, the BSE small cap

recorded a surge of 1.10 per cent.

During

the week under review, FIIs have remained net buyers of equities to the

extent of Rs 568 crore with purchases of Rs 5939 crore and sales of Rs

5372 crore, while mutual funds have turned net sellers to the extent of Rs

56 crore with sales of Rs 2628 crore and purchases of Rs 2572 crore.

As

per Financial Express research bureau, the

National

Securities Depositories Ltd (NSDL) has said that if a depository

participant (DP) opens a account without adequate proof of residence or

identity or without conforming to the NDSL rules then a penalty of Rs

5,000 would be charged and if two such deviations were observed then the

amount of penalty would increase.

Derivatives

The

daily average turnover of futures and options segment of NSE has increased

from Rs 19,537 crore in the week ended August 18 to Rs 22,533 crore in the

week under review.

Government

Securities Market

Primary

Market

RBI

conducted auction of state development loans with 10-year maturity for

four states for an aggregate amount of Rs 1050 crore at a cut-off of 8.11

per cent.

The

cut-off yield set at the 91-day Treasury bill has remained steady at 6.40

per cent in the auction held on August 23, while that of 182-day TB has

risen to 6.72 per cent from 6.69 per cent set in the previous week.

Secondary

Market

RBI

has authorised three more banks, Hongkong and Shanghai Banking Corportaion

Ltd, Bank of America and J P Morgan Chase Bank to undertake primary

dealership with effect from August 28, 2006; concomitantly, the

authorization given to HSBC primary dealership (India) Private Limited,

Bank of America Securities (India) Pvt Ltd and J P Morgan Securities India

Private Ltd as primary dealers stands withdrawn.

Despite

the rising inflation rate, the weighted average YTM of 7.59 per cent 2016

has fallen from 8.03 per cent on August 18 to 7.94 per cent on August 25

as the international oil prices have eased.

Bond

Market

During

the week, two banks, one financial institution and a central government

undertaking have tapped the market to mobilise Rs 1,400 crore.

Foreign

Exchange Market

RBI

has permitted scheduled commercial banks (SCBs) to offer internet based

foreign exchange services in addition to the local products already

allowed to be offered on internet based platforms subject to terms and

conditions.

During

the week, the rupee has depreciated from Rs 46.48 on August 18 to Rs 46.61

on August 25, while the six-month forward premia has declined to 1.31 per

cent on August 25 from 1.43 per cent on August 18.

Commodities

Futures derivatives

Forward

Market Commission (FMC) has circulated a draft guidelines among exchanges

seeking their views to facilitate the launch of portfolio management

services (PMS) in commodities. Indication are that PMS would be on the

same lines as that in equities with such services being offered to high

net worth individuals.

Insurance

Bharati

AXA Life Insurance Company Ltd has started its operations with the opening

of its first branch office in

Corporate Sector

According to Reserve Bank of India (RBI) data, overseas borrowings by Indian companies have increased by 91 per cent to $ 4.43 billion in the first quarter of the current (Q1) fiscal year from $ 2.23 billion a year ago. As per RBI, during Q1 2006-07, corporates have mobilised $ 2.22 billion through external commercial borrowings (ECBs), up 28 per cent from Q1 2005-06 and $ 2.21 billion through foreign currency convertible bonds (FCCBs), up 273 per cent. The data shows that the companies have planned to use FCCB and ECB loans for various purposes like modernisation of existing facilities, new projects and import of capital goods.

|

Table:

Top ECB/FCCB borrowers in Q1 2006-07 ($ million) |

|||

|

Borrower |

ECB |

Borrower |

FCCB |

|

MMD

Health Care |

300 |

Amtek

Auto |

250 |

|

Indian

Farmers and Fertilisers |

246 |

Reliance

Natural Resources |

250 |

|

Kingfisher

Airlines |

126 |

Jubilant

Organosys |

200 |

|

Essar

Steel |

120 |

Mah

and Mah |

200 |

|

Bharti

Airtel |

102 |

Aurobindo

pharma |

150 |

|

Source:

RBI (www.rbi.org.in) |

|||

Engineering

and construction company Punj Lloyd has secured an order worth over Rs

1,347 crore ($ 290 million) from

Construction company Patel Engineering Limited has received an order of Rs 318 crore from National Thermal Power Corporation (NTPC) for a 600-MW hydro power project in Uttaranchal.

KEC

International Limited has received three orders worth Rs 150 crore from

international and domestic markets. GRTE, the power transmission division

of Algerian company Sonelgaz, has placed Rs 70 crore order for supply and

construction of 400 kv single circuit transmission line over 52 km from

Ain Sefra to Mougrar. The West Bengal State Electricity board has placed

Rs 58 crore order for construction of three lines of 132 kv each around

Haldia. The company has also received Rs 22 crore contract in

Bharat Forge and the Maharashtra government has signed a memorandum of understanding to set up a multi-product special economic zone (SEZ), spread over 2,000 hectares at Khed in Pune with an initial investment of Rs 2,000 crore. The state government will hold 24 per cent equity through its industrial infrastructure arm, Maharashtra Industrial Development Corporation (MIDC). The SEZ is likely to attract the investment of around Rs 25,000 crore and create around 1.20 lakh jobs in the region.

Tata Tea Limited and its promoter Tata Sons have jointly acquired 30 per cent shares in Energy Brands Incorporate a US based company, for around Rs 3148 crore ($ 677 million).

Punj

Lloyd has formed a joint venture with Kaefer Insulation of Germany to set

up a large cold chain network across

Pulp and paper manufacturer Ballarpur Industries Limited (BILT) has registered an increase of 67.7 per cent in net profit to Rs 67.9 crore for the quarter ended June 2006. The company’ sales revenue has risen by 8.7 per cent to Rs 571.35 crore from Rs 525.35 crore in the corresponding period a year ago. The sales revenues have been helped by growth in sales of paper and paper product, which grown by 15.8 per cent to Rs 477.5 crore. For the year ended June 2006, BILT has reported a growth of 26.2 per cent in its net profit to Rs 212 crore from Rs 168 crore.

Telecom

In

one of the biggest network management and rollout deals globally,

![]()

|

Macroeconomic Indicators |

|

Table

1 : Index Numbers of Industrial Production (1993-94 =100) |

|

Table

2 : Production in Infrastructure Industries (Physical Output Series) |

| Table 3: Procurment, Offtake and Stock of foodgrains |

|

Table

4: Index Numbers of Wholesale Prices (1993-94 = 100) |

|

Table

5 : Cost of Living Indices |

|

Table

6 : Budgetary Position of Government of India |

|

Table

7 : Government Borrowing Programmes and Performance |

|

Table

8 : Scheduled Commercial Banks -

Business |

|

Table

9 : Money Stock : components and Sources |

|

Table 10 : Reserve Money : Components and Sources |

|

Table

11 : Average Daily Turnover in Call Money Market |

|

Table

12 : Assistance Sanctioned and Disbursed by All-India Financial

Institutions |

|

Table

13 : Capital Market |

|

Table

14 : Foreign Trade |

|

Table 15 : India's Overall Balance of Payments |

|

Table

16 : Foreign Investment Inflows |

| Table 17 : Foreign Collaboration Approvals (Route-Wise) |

| Table 18 : Year-Wise (Route-Wise) Actual Inflows of Foreign Direct Investment (FDI/NRI) |

|

Table

19 : NRI Deposits - Outstandings |

|

Table

20 : Foreign Exchange Reserves |

|

Table 21 : Indices REER and NEER of the Indian Rupee |

|

Table

22 : Turnover in Foreign Exchange Market |

| Table 23 : India's Template on International Reserves and Foreign Currency Liquidity [As reported under the IMFs special data dissemination standards (SDDS) |

| Table 24 : Settlement Volume and Netting Factor for Government Securities Transactions Settled at CCIL - Monthly, Quarterly and Annual Basis. |

| Table 25 : Inter-Catasegory Distribution of All Types of Trade in Government Securities Settled at CCIL (With Market Share in Respective Trade Types) |

| Table 26 : Category-wise Market Share in Settlement Volume of Government Securities Transactions (in Per Cent) |

| Table 27 : Settlement Volume and Netting Factor for Total Forex Transactions Settled at CCIL - Monthly, Quarterly and Annual Basis. |

| Table 28 : Inter-Category Distribution of Total Foreign Exchange Transactions Settled at CCIL (With Market Share in Respective Trade Types) |

![]()

|

Memorandum Items |

*These statistics and the accompanying review are a product arising from the work undertaken under the joint ICICI research centre.org-EPWRF Data Base Project.

We will be grateful if you could kindly send us your feed back at epwrf@vsnl.com